French OG

April 4, 2025

I know I should not be "shooting the ambulance", but...

I decided to look into Bumble's recent 10K filing out of curiosity, plus I did some research to analyse the stock and see how bad the situation was, and this is what I found:

1. The Average Revenue Per User decreased from $23.01 in Q4 2022 to $22.64 in Q4 2023 to $21.17, slightly higher than $21.12 in Q4 2021.

2. Lots of Money is wasted on Marketing with no game-changing initiatives.

3. Awful financials. No wonder the CFO left.

4. It does not take a financial wizard to see how little growth there is. At the same time, the write-downs of rubbish investments (Fruitz App and their 2021 and 2022 stock buybacks) impacted their financial health through their impairment loss—talking about enhancing stockholders' value.

5. Despite their best non-GAAP efforts, even the macro environment, which is positive for Tech, has not benefited them.

6. The current ratio slightly improves, which means the company can meet its short-term liabilities. However, the impairment loss affected the Goodwill and Intangible Assets section badly, illustrating the 30% drop in the value of their Assets.

7. The D/E ratio increased year over year and was above the industry average. Bumble's position is fragile, as more than 50% of its Assets are intangibles. While it is usual for tech companies to have a much higher percentage, Bumble's is higher than aggressive tech stocks.

8. Net Income is not as crucial as Cash Position regarding Tech Stocks, but the trend is not Bumble's friend. They went from $281 million in Net Income to $767 million in Net Losses in 3 years. A $1 billion delta is not something to ignore.

9. Now, let's look at the Free Cash Flow. They make less from operating activities than in previous years, and despite lower CAPEX, they are still behind the 2022 numbers. Their FCF Margin has decreased by about 30%, showing a shrinking proportion of revenue that becomes FCF.

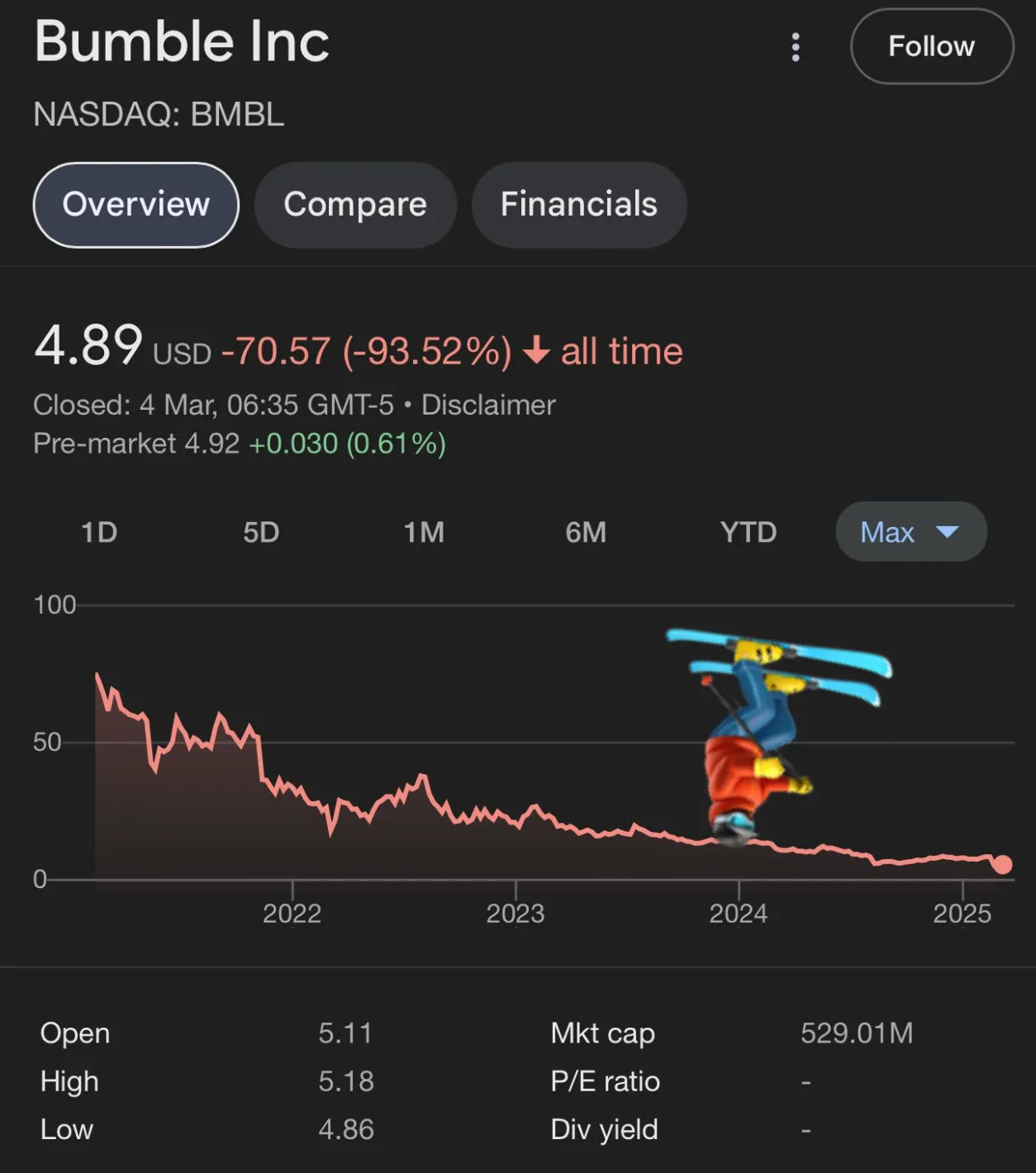

10. What about Enterprise Value? Enterprise Value decreased from $2.25 billion in 2021 to $829 million, a 64% drop in the space of three years. Ooooooof.

EV/EBITDA 2022: 13.98x

EV/EBITDA 2023: 8.28x

EV/EBITDA 2024: 3.98x

Industry average: 14x-16x

Save Private Bumble.

11. Are you telling me the situation could be worse than what is already on file? Oh, Lord. Considering the previous CFO resigned at the end of November, we would call this a red flag in the dating world. Let's see if there is a change of fortune with the former CEO returning.

12. It is a tech company, and we must examine its growth prospects. The market has already priced most, if not all, of the above. So, what are the plans to change course?

- Enhancing User Experience by implementing mandatory picture uploads and ID verification to improve user trust and safety. This safety approach is very much a female-driven approach that adds little value. It is not going to address catfishing.

- Introducing AI-driven features. Upcoming features include an AI photo picker and enhanced ID verification processes. It's hardly something that is going to change anything.

- Streamlining the App’s Portfolio to focus on Bumble's core applications. Bumble intends to discontinue smaller platforms like Fruitz and Official in 2025 to strengthen its ecosystem and improve customer experiences. Although this incurred a loss, it makes sense.

- Rebalancing marketing strategies by adjusting its marketing approach to drive high-quality user growth, focusing on acquiring users more likely to engage and convert into paying customers. Sounds like wishful thinking.

- I noticed that they also added a discovery tab. It should curate profiles better suited to your tastes and match your relationship expectations. From what I have seen, there is little relevance.

13. How will they use their cash outside the "product enhancement and marketing optimisation" above?

a. They have announced a $450 million stock buyback program…As if the previous impairment was not a warning to heed, they are doubling down on it.

It sounds like your typical past-her-prime woman on their app doubling down on her requirements, although they don't have the leverage to do so.

The Hive Mind does not care.

MANIFEST QUEENS!!!!

Not everyone is Jay Powell, but they think they are. Short Sellers rise.

b. To maintain financial flexibility, Bumble extended the maturity date of its revolving credit facility to June 17, 2026, to ensure continued access to capital for operational needs and potential strategic investments.

At this point, why not go all in?

14. Considering all of the above and whilst not having exhaustively analysed the financials, Bumble is in a make-or-break situation where it needs to make a much bigger gamble in a saturated market, not some satellite changes, if it wants to remain relevant.

Still, they are looking at some financial chicanery taught in the usual MBSA schools.

Below, we see the forward guidance from management. This represents a 7% to 10% drop in YoY Revenue and an Adjusted EBITDA drop from $74 million in Q1 2024.

Bonus: Do you see a change in the trend for the Technical Analysts out there?